When you buy life insurance, you aren’t just buying a paper contract. You are buying a promise. You are telling your spouse, your children, and your future self: “If the worst happens, you will be taken care of.”

That promise might need to be kept 20, 30, or even 50 years from now.

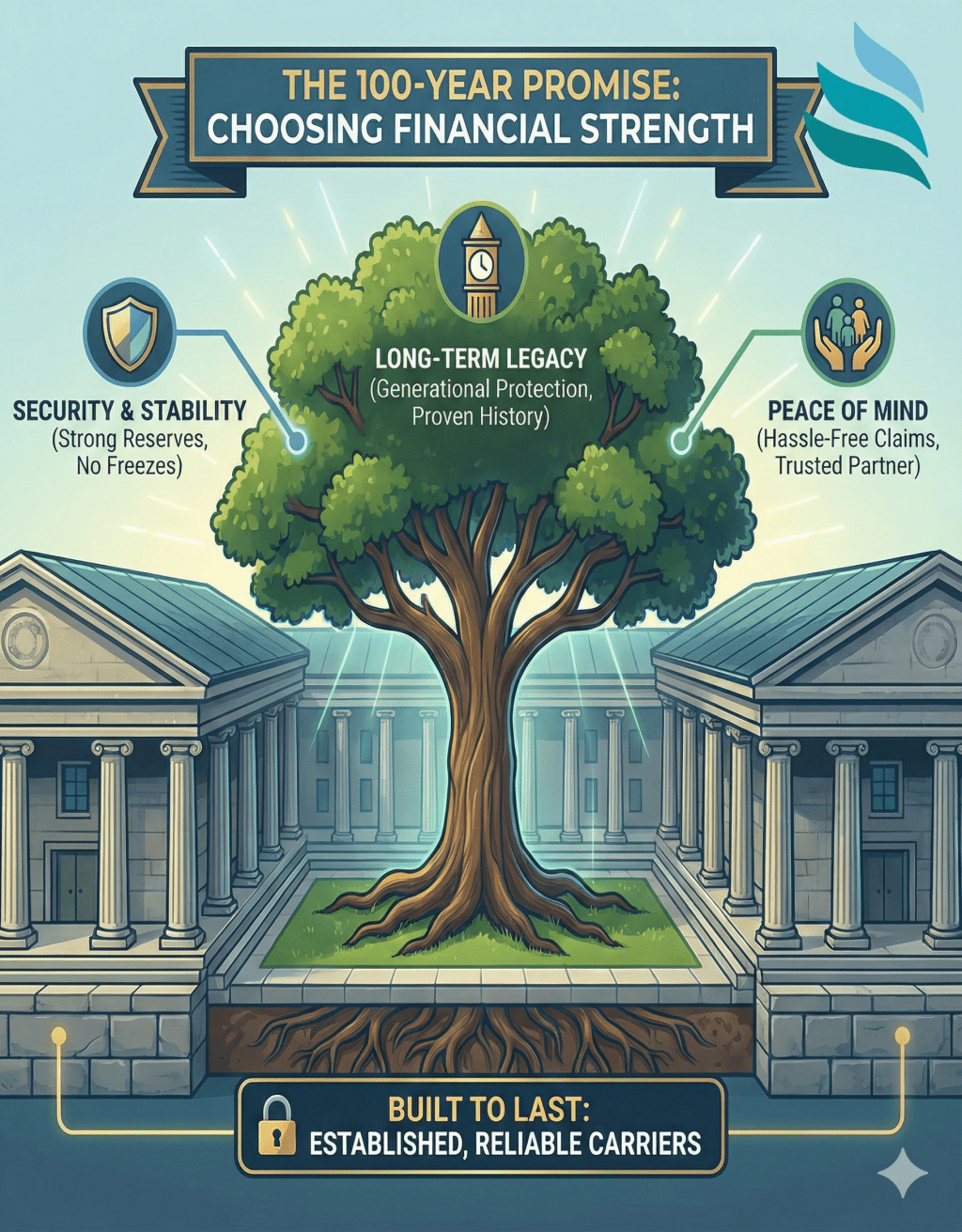

In a world full of startups, spinoffs, and “disruptors,” it is tempting to go with a smaller, newer company that might offer a slightly cheaper premium or a flashier website. But when your family’s financial survival is on the line, there is a distinct advantage to choosing a company that has weathered the storms for over a century.

Here is why choosing a top-tier, heritage company isn’t just about brand names it’s about eliminating risk and hassle for the people you love.

The Hidden Risk of “Small and New”

We often think of insurance risk in terms of us dying. But there is another risk: the company dying.

While it is true that the industry has a safety net (State Guaranty Associations) to prevent total catastrophe, relying on that net is not a smooth experience. If a smaller, less capitalized insurer hits a financial wall like many did during the 2008 crisis your policy doesn’t just seamlessly switch over.

If you choose a smaller or struggling carrier, here is the baggage you might be leaving for your family:

- The “Frozen” Asset: When companies like Standard Life of Indiana failed, regulators froze assets. If you had cash value you intended to use for a child’s tuition or an emergency, it was locked away for over a year. A large, solvent company doesn’t freeze your money.

- The Administrative Nightmare: When a company like Shenandoah Life went into receivership, policyholders spent three years in limbo. Imagine your beneficiaries trying to file a claim, only to find the company is being run by a government receiver, customer service is non-existent, and the payout is delayed.

- The “Spinoff” Shuffle: Small spinoffs are often sold and resold. Your policy might start with “Company A,” get sold to “Company B,” and end up administered by “Company C.” Each time, you lose that relationship with your trusted agent, logins change, and paperwork gets lost.

The Comfort of the Giants

Corebridge Financial owns and operates American General Life, which has been around for over 100 years. Corebridge was created by AIG and is still partially owned by AIG today. They operate with massive financial reserves designed to absorb shocks that would shatter smaller companies.

When you choose a top-tier carrier, you are paying for Continuity.

- They Pay When it Matters: During the 2008 crisis, while smaller insurers were being liquidated, the top rated companies were not only paying claims instantly they were paying dividends to their policyholders.

- One Call Resolution: If your family ever has to make that claim, they shouldn’t have to navigate a liquidation court. They should be able to call a recognizable name, speak to a professional, and receive their funds quickly.

Peace of Mind is Worth it

When you choose a major, highly rated insurer, you are ensuring that the administrative burden on your family is near zero. You are ensuring that the check clears, your agent answers the phone, and the promise you made is kept without a single hiccup.

Leave a comment